TipRanks Smart Growth Portfolio #12: Margin Code

1

Dear Investors,

Welcome to the 12th edition of the Smart Growth Portfolio and Newsletter.

1

1

Portfolio News

❖ GitLab (GTLB) has secured FedRAMP Moderate Authority to Operate (ATO) for its “GitLab Dedicated for Government” platform, a key certification that clears the way for use across U.S. federal agencies. Sponsored by the General Services Administration, the approval confirms GitLab meets strict security and compliance standards required to handle sensitive government workloads.

FedRAMP authorization is a major gatekeeper for cloud vendors aiming to serve the $12B+ federal IT market. With this milestone, GitLab joins a select group of providers eligible for government contracts. The certified platform delivers a single-tenant DevSecOps environment with private networking and continuous monitoring, features tailored for regulated environments like defense and intelligence.

This move strengthens GitLab’s public sector push and positions it as a credible competitor to GitHub Enterprise and others. While near-term revenue impact may be modest, the long-term strategic value is significant as GitLab targets broader adoption in mission-critical settings.

1

❖ Morgan Stanley has reaffirmed its bullish stance on Nutanix (NTNX), maintaining a “Buy” rating and raising the price target to $90 from $75. Morgan Stanley’s note cited strong performance trends across enterprise storage stocks (including NTAP, HPE, NTNX, etc.), noting the group is up over 10% since early April. This context sets the stage for their view that expectations may now be elevated heading into Q1 earnings, which could create a challenging setup if results don’t exceed the optimism. Despite this, Nutanix is called out as their most encouraging pick within the group, reflecting company-specific strength rather than just sector momentum.

1

❖ Powerfleet (AIOT) released preliminary Q1 2025 results ahead of its May 28 earnings call, showing continued strength following its merger with MiX Telematics. The company expects revenue between $60.0-60.4 million and adjusted EBITDA of $6.2-6.4 million, reflecting operational momentum and accelerating synergy realization. Cost synergies hit a $15 million annual run-rate by quarter-end, well ahead of prior projections. CEO Steve Towe emphasized a focus on margin expansion and efficient integration. Net debt declined to $99.2 million, with $27.6 million in cash. Full earnings results will be released on May 28.

As PowerFleet enters fiscal 2026, it expects total revenue to grow by 20-25% and adjusted EBITDA to rise by 45-55%, even as tariff-related pressures and slower customer decision-making create some uncertainty. While these external factors have led the company to take a more cautious tone, its core operations remain strong. Importantly, the growth forecast is based on an adjusted revenue baseline of $352.5 million – about 3% lower than the estimated actual FY25 revenue – due to a change in how hardware sales are accounted for under U.S. GAAP and the discontinuation of certain legacy FSM revenue.

1

1

This Week’s Top Growth Pick: ACI Worldwide (ACIW)

ACI Worldwide Inc. is a global payments software provider powering mission-critical transactions for banks, merchants, and billers. Best known for its enterprise-grade payment solutions, ACI has steadily repositioned itself as a leader in intelligent payment orchestration – offering flexible, real-time capabilities that help customers modernize their payment infrastructure. Its platform spans multiple use cases, from digital banking and merchant acquiring to bill payment and fraud prevention. With a clear focus on recurring software revenue and operational efficiency, ACI is quietly becoming a key infrastructure player in the accelerating shift toward real-time digital payments. As global demand rises for secure, scalable, and interoperable payments technology, ACI’s role at the intersection of financial institutions and next-gen payment rails positions it well for sustainable growth.

Source: ACI Worldwide, Inc. Factsheet

1

Protocol Shift

Founded in 1975, ACI Worldwide started as an innovator in electronic transaction processing, best known for its BASE24 platform that powered early ATM and card networks. Over the years, ACI expanded globally, went public in the mid-1990s, and steadily evolved into a broader payments software provider. But the company’s most meaningful transformation has occurred over the past several years.

A key inflection point came in 2019 with the $750 million acquisition of Speedpay from Western Union – a move that doubled ACI’s billing business and laid the foundation for a more diversified revenue model. Since then, ACI has focused on scaling its enterprise-grade payment software while pivoting toward real-time payment orchestration, a fast-growing segment fueled by the rise of instant digital transactions.

Between 2020 and 2024, the company invested heavily in modernizing its platform and expanding its global reach. That included real-time payments initiatives in India and Brazil, and deepened partnerships with players like Mastercard and Banfico (a U.K. fintech specializing in payment and identity verification) to accelerate rollout in high-growth corridors. ACI also embedded its technology into new verticals like healthcare payments and government disbursements via partnerships with NationsBenefits and others.

Alongside organic investments, ACI has worked to unify and streamline its product architecture. In 2024, it merged its Bank and Merchant segments into a single Payment Software unit – a strategic move aimed at simplifying its go-to-market approach and aligning behind its high-margin software portfolio. This was coupled with a sharpened focus on recurring revenue, margin expansion, and cash flow generation.

What began as a transaction processing firm is now positioned as a global software layer for real-time, intelligent payments. With an expanding roster of bank and enterprise customers, a more flexible product stack, and a growing presence in key real-time markets, ACI is shifting from legacy payments processor to strategic enabler of modern digital finance. The groundwork laid over the past five years has put the company on a more scalable, software-first path – and set the stage for meaningful long-term growth.

Source: ACI Worldwide, Inc. Investor Presentation, Spring/Summer 2025

1

Stream Engine

ACI Worldwide has redefined itself as a modern payments software provider – a SaaS-first business delivering mission-critical infrastructure to banks, merchants, and billers around the globe. While its roots lie in legacy transaction processing, ACI’s evolution has centered on one core idea: intelligent payment orchestration. In a fragmented, always-on payments world, orchestration means managing every moving part – payment methods, processors, networks, geographies, compliance, and risk – through a single, streamlined platform.

That’s where ACI sets itself apart. Its orchestration engine doesn’t just connect endpoints – it optimizes flows. Transactions are smart-routed to the best-performing acquirer, failed payments are automatically retried, fraud checks run in parallel, and settlement preferences are enforced – all in real time. This complexity is shielded from the end user, but it’s nevertheless what drives higher approval rates, fewer chargebacks, and better conversion.

Equally important is ACI’s fraud orchestration suite – a powerful layer that merges device intelligence, behavioral analytics, and machine learning to stop bad actors before they strike. Rather than relying on rigid rules or siloed fraud tools, ACI’s platform dynamically evaluates risk in real time across all channels. The company was recently recognized as a leading global provider in this space, validating its strategic push to make fraud prevention smarter, faster, and more adaptive.

ACI’s product stack supports this orchestration through three main revenue streams. The largest and fastest-growing is its cloud-based Software-as-a-Service (SaaS) and Platform-as-a-Service (PaaS) offerings – recurring revenue services that power digital banking, fraud detection, bill payments, and real-time payments. This segment now represents the bulk of new business and customer expansion.

Traditional on-premises software still plays a role, too. ACI licenses its software to large institutions that prefer internal hosting, generating a stable mix of upfront license and recurring maintenance revenue. While this stream has matured, it continues to support long-standing enterprise relationships.

The third stream is services – including system integration, onboarding, and optimization. These services don’t drive growth on their own, but they support stickiness by embedding ACI more deeply in clients’ tech stacks.

ACI’s recurring revenue footprint has grown meaningfully over the past five years, reflecting a deliberate pivot toward high-margin, predictable software sales. Its orchestration focus gives it an edge over point-solution rivals that lack breadth – while its institutional scale and global coverage distinguish it from younger fintech upstarts.

In short, ACI isn’t just processing payments anymore. It’s coordinating them – across systems, rails, and regions – with the precision and reliability modern finance demands. And in an era where real-time, secure, and seamless payments are no longer optional, that role is increasingly central.

Source: ACI Worldwide, Inc. Investor Presentation, Spring/Summer 2025

1

Buffered Profits

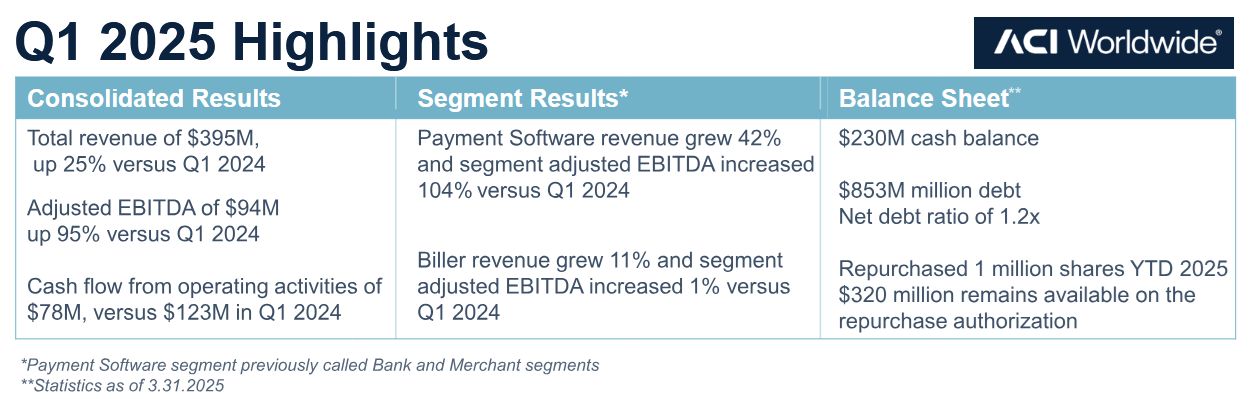

ACI Worldwide reported a strong opening quarter for fiscal 2025, beating internal targets and lifting its full-year guidance on the back of accelerating growth in its core Payment Software segment. Total revenue for Q1 rose 25% year-over-year to $395 million, surpassing both the company’s expectations and typical seasonal benchmarks.

Recurring revenue – from SaaS, PaaS, and maintenance – reached $286 million, up 8% year-over-year, and made up 72% of total revenue, a signal that ACI’s SaaS-first strategy is delivering results. The standout performer was the Payment Software unit, which grew segment revenue by 42% and segment-adjusted EBITDA by 104% YoY, fueled by strong demand from large banks modernizing their issuing and acquiring systems. Meanwhile, the Biller segment – still a major contributor – grew revenue by 11%, maintaining stable EBITDA margins, with new ARR bookings up about 40% over Q1 2024.

Net income came in at $59 million, a sharp reversal from an $8 million loss in the year-ago period. This included a $22 million after-tax gain from the sale of ACI’s minority stake in Mindgate, an India-based real-time payments platform. Excluding this one-time gain, adjusted EBITDA nearly doubled YoY to $94 million, with net adjusted EBITDA margin expanding to 36%, up from 24% last year. GAAP earnings per share came in at $0.55, up sharply from a $0.07 loss in Q1 2024, while adjusted EPS rose to $0.51 from $0.10 – a more than fivefold increase.

Free cash flow, however, dipped slightly – $78 million versus $123 million in Q1 2024 – due to changes in working capital and timing of tax payments. Still, the company ended the quarter with $230 million in cash and a net debt leverage ratio of just 1.2x, signaling a strong balance sheet and room for both investment in growth and buybacks.

Looking ahead, management raised full-year revenue guidance to $1.690-1.720 billion, up from a prior range of $1.685-1.715 billion. Adjusted EBITDA guidance was reaffirmed at $480-495 million, with Q2 revenue projected at $375-385 million and Q2 EBITDA between $55-65 million. Current analyst consensus sits near the midpoint of these ranges, suggesting the company remains in line to meet or modestly exceed Wall Street expectations.

In Q1, the company not only cleared the “Rule of 40” – it smashed through it, delivering 25% revenue growth and a 36% adjusted EBITDA margin. The combined score of 61% signals rare operating efficiency, especially in fintech infrastructure. With 72% of revenue now recurring and ARR bookings on the rise, this “Rule of 40” beat is no anomaly – it reflects underlying structural momentum. ACI’s disciplined shift toward SaaS, real-time payments, and fraud orchestration is driving not just top-line acceleration but real bottom-line leverage as well.

Source: ACI Worldwide, Inc. Q1 2025 Earnings Presentation

1

Low Latency, High Upside

ACI’s stock – like many growth and technology stocks – has come under pressure this year, declining by about 11% year-to-date, but still doing better than most of its peers in the industry. In fact, among all peers, ACIW has only underperformed Fidelity National Information Services – a large-cap perceived as a defensive play – year-to-date. Despite this year’s weakness, ACI’s stock is up about 27% over the past 12 months, outperforming broad indexes as well as nearly all peers.

Currently, ACIW is trading at compelling valuation levels. Its TTM and forward non-GAAP P/E multiples carry a discount of about 25% to Technology sector averages, while EV/EBITDA (TTM and forward) is about 20% below average, and EV/Sales is roughly in line with the sector. Versus peers in the industry, ACI’s stock sits at or near the bottom of the valuation range on all these metrics – despite the fact that its growth and profitability balance arguably justifies a premium multiple. Based on projected free cash flows, the stock appears to be undervalued by roughly 40%, offering an attractive entry point for long-term growth investors.

Beyond potential price appreciation, ACI continues to reward shareholders through active buybacks. In June 2024, the company’s board approved a $400 million share repurchase program, which included the remaining $65 million from its prior authorization, with no expiration date. In 2024, ACI repurchased approximately 4 million shares for $128 million, and added another 1 million shares worth $52 million in Q1 2025. At the end of the quarter, the company had approximately $320 million remaining under the current authorization.

Wall Street remains bullish: analysts currently rate ACIW a “Strong Buy,” with a 12-month average price target implying more than 49% upside from current levels.

For investors seeking resilient infrastructure plays with real earnings power, ACI is a rare find – priced like a laggard, performing like a leader. As market sentiment stabilizes and fundamentals continue to strengthen, ACIW looks well-positioned to rerate upward – with buybacks and real cash flow adding fuel to the rebound.

1

To Sum It All Up

ACI Worldwide is a mission-critical fintech infrastructure provider powering real-time payments, fraud prevention, and digital biller services across banks, merchants, and enterprises. With a deliberate pivot to a SaaS-first model, ACI now generates the majority of its revenue from recurring software and platform services. Its intelligent orchestration engine and fraud stack give it a strategic edge in the shift toward faster, smarter, and more secure payments. The company has streamlined operations, expanded its global reach, and deepened partner integrations, all while maintaining financial discipline and cash generation. For investors seeking efficient growth in enterprise fintech, ACI offers a differentiated platform play with both structural upside and rerating potential.

1

1

Smart Growth Portfolio

|

1

1

Click here for more stock analysis from TipRanks Macro & Markets research analyst Yulia Vaiman

1

Disclaimer

The information contained in this article represents the views and opinions of the writer only, and not the views or opinions of TipRanks or its affiliates and should be considered for informational purposes only. TipRanks makes no warranties about the completeness, accuracy, or reliability of such information. Nothing in this article should be taken as a recommendation or solicitation to purchase or sell securities. Nothing in the article constitutes legal, professional, investment and/or financial advice and/or takes into account the specific needs and/or requirements of an individual, nor does any information in the article constitute a comprehensive or complete statement of the matters or subject discussed therein. TipRanks and its affiliates disclaim all liability or responsibility with respect to the content of the article, and any action taken upon the information in the article is at your own and sole risk. The link to this article does not constitute an endorsement or recommendation by TipRanks or its affiliates. Past performance is not indicative of future results, prices, or performance.