TipRanks Smart Growth Portfolio #23: Payback Time

Dear Investors,

Welcome to the 23rd edition of the Smart Growth Portfolio and Newsletter.

1

1

Portfolio Updates

❖ ❖ ❖ We are happy to announce the addition of MKS Inc. (MKSI) – which was recommended in one of our previous Newsletters – to the Smart Growth Portfolio.

MKS is a vertically integrated technology platform supplying the precision photonics, vacuum, power, and specialty chemical systems that enable the most advanced manufacturing processes in semiconductors, electronics, and specialty industrial markets. Its reach spans wafer fabrication, advanced packaging, aerospace, defense, and life sciences – giving it exposure to multiple secular growth drivers, from AI datacenters to satellite communications. The 2022 acquisition of Atotech added a high-margin, recurring specialty chemicals business, transforming MKS into one of the few companies able to deliver full-stack process solutions across the semiconductor lifecycle.

Q2 2025 results reinforced this transformation. Revenue rose to $973 million, surpassing the high end of guidance and consensus estimates, with broad-based strength across Semiconductor and Electronics & Packaging. Adjusted EBITDA climbed to $240 million – a margin of 24.7% – while GAAP net income reached $62 million. Non-GAAP EPS came in well above the midpoint of guidance, extending a streak of consensus beats in every quarter since Q2 2021. Notably, recurring consumables and services now represent nearly 40% of revenue, providing a more stable earnings base.

Management is executing with discipline. In addition to operational momentum, MKS prepaid $200 million in debt in Q2 and early Q3, further reducing leverage while maintaining a $674 million cash balance and full revolver access. Gross margins remain robust despite tariff headwinds – projected at 46.5% for Q3 – as product mix shifts toward higher-value systems and chemicals.

The market has begun to recognize this resilience, with shares up more than 60% from April lows. Still, MKSI trades below peers on forward EV/EBITDA, while its PEG ratio of 0.82 suggests a “growth at a reasonable price” setup. Analysts rate the stock a “Strong Buy,” with an average target implying nearly 20% upside from current levels. While detailed post-earnings revisions are still unfolding, early signs suggest that analysts may revisit their estimates to reflect the company’s accelerating execution and improved outlook.

For long-term growth investors, MKS offers rare leverage to AI-driven semiconductor demand, advanced packaging adoption, and the ongoing re-architecture of global electronics supply chains – all underpinned by improving margins, strong cash flow, and a deliberate balance sheet strategy. In short, this is an enabler of the enablers, with the fundamentals and valuation to match.

1

❖ ❖ ❖ After careful consideration, we have decided to sell Alkami Technology (ALKT). This decision follows another disappointing quarter and a collapse in sentiment that leaves little near-term recovery potential. The stock is down about 43% year-to-date after ALKT missed non-GAAP EPS expectations for three consecutive quarters – a pattern that has eroded confidence in management’s execution and forecasting.

Alkami’s Q2 2025 revenue rose 36% year-over-year to $112.1 million, exceeding estimates by $2.09 million, driven by strong subscription growth and the integration of MANTL. Adjusted EBITDA jumped 159% to $11.9 million, highlighting operational leverage. ARR climbed 32% to $424 million, with registered users up 2.3 million from a year ago to 20.9 million. However, the company posted a GAAP net loss of $0.13 per share versus expectations for a $0.08 profit – a 262% downside surprise – driven by rising R&D, stock-based compensation, and integration costs. Non-GAAP EPS came in at $0.02 versus the expected $0.08, down 55% YoY.

While the company’s revenue growth is stellar and its ARR expansion plus user base gains are outstanding even for a fintech SaaS, the market is punishing the path it’s taking to get there. Missing on EPS for three quarters in a row sends the signal that either cost discipline is absent or management can’t accurately forecast – eroding institutional confidence. The market’s reaction was swift and severe, with shares dropping on results and extending a months-long downtrend. Analyst sentiment has softened further in recent weeks, with no upgrades since March and multiple price target cuts.

Guidance failed to restore confidence. Q3 revenue is projected at ~$113.3 million versus the Street’s $116 million outlook, while full-year revenue of $445 million and adjusted EBITDA of $52.8 million both sit at midpoints that imply no upward momentum. In the current macro and market conditions, investors are rewarding growth with earnings beats and free cash flow – not “growth-at-all-costs” models. Light revenue guidance, even with improving EBITDA, suggests the growth/profitability crossover is farther away than hoped.

Although MANTL integration and R&D push could pay off long-term, the market isn’t pricing for eventual payoffs at the moment. It’s rewarding near-term execution, clear earnings beats, and free cash flow generation – all things Alkami is not delivering right now. Given that ALKT isn’t cheap despite YTD underperformance, investor skepticism appears warranted. The large year-to-date loss and thin liquidity amplify each negative surprise, and sentiment rarely turns quickly in such cases. It usually requires at least one “beat-and-raise” report to reverse the narrative – meaning more drawdown risk before that happens.

While Alkami’s product adoption remains strong and its long-term positioning in digital banking is compelling, the road to profitability is lengthening and sentiment is firmly negative. Without a major catalyst, a sustained rebound in the near term looks unlikely. We prefer to exit now, preserve capital, and monitor from the sidelines for any future execution turnaround.

1

1

Portfolio News

❖ Monday.com (MNDY) is scheduled to report its Q2 2025 earnings on August 11. Two other Portfolio stocks that are yet to release their quarterly results are Nutanix (NTNX) and Micron (MU), with the reporting dates on August 27 and September 25, respectively.

1

❖ EverQuote (EVER) reported a strong Q2 2025, beating expectations across revenue and profitability while setting new quarterly records. Total revenue grew 34% YoY to $156.6 million – with the core automotive insurance vertical up 36% and home and renters up 23%. While revenue came in just shy of the Street’s $157.2 million consensus, adjusted EBITDA of $22.0 million and net income of $14.7 million both handily outperformed, with EPS of $0.40 marking a 122% increase from last year. This was the company’s highest Q2 net income since going public – fueled by a 25% rise in variable marketing dollars and improved operating leverage.

Record operating cash flow of $25.3 million and a 19% sequential increase in cash to $148.2 million further strengthened the balance sheet. In response, management announced a $50 million inaugural share repurchase program – underscoring confidence in the company’s financial position and long-term growth. EverQuote also reaffirmed its path toward $1 billion in annual revenue – a multi-year goal supported by rising carrier spend, product expansion, and ongoing platform improvements.

Management commentary emphasized EverQuote’s execution in leveraging data and AI – particularly voice agents and ML-driven smart campaigns – to boost efficiency and partner performance. One large enterprise carrier increased its spend by 61%, showing renewed momentum, but the company also flagged headwinds. A few carriers are still pacing cautiously, balancing growth with efficiency after prior underwriting losses. In parallel, certain geographies – most notably California – remain slow to recover due to regulatory bottlenecks and tighter market conditions, with full normalization not expected before year-end.

Looking ahead, EverQuote guided for Q3 revenue of $163-169 million (15% YoY growth at the midpoint) and adjusted EBITDA of $22-24 million (22% growth), both above prior internal forecasts. Analysts responded positively, with several reaffirmed “Buy” ratings and no downgrades. While the stock dipped post-earnings, historical patterns suggest strong 30-day follow-through after beats – aligning with EverQuote’s current momentum and tech-driven trajectory.

1

❖ Clear Secure (YOU) posted a mixed Q2 2025, with strong revenue growth and member gains offset by a notable EPS miss. Revenue rose 17.5% YoY to $219.5 million, beating consensus of $215 million, driven by robust travel activity and record CLEAR Plus usage. Total bookings climbed 13.1% to $222.9 million, while free cash flow hit $117.9 million – reinforcing the company’s ability to self-fund growth. Active CLEAR Plus membership reached 7.6 million (+7.5% YoY), supported by international expansion into the UK, Canada, Australia, and New Zealand. Total members grew 38% YoY to 33.5 million.

EPS came in at $0.26, missing the Street’s $0.31 estimate, a shortfall attributed in part to higher investment in product innovation and global rollout. Still, investors reacted positively, with shares jumping after the release on optimism around top-line momentum and strategic initiatives.

Product launches during the quarter included CLEAR Concierge at 14 airports and the rollout of EnVe enrollment pods and ePassport capabilities – all geared toward increasing CLEAR’s addressable market and deepening user stickiness. Notably, the company maintained 87.3% gross dollar retention even as CLEAR Plus pricing rose to $209 for individuals and $125 for family plans. CEO Caryn Seidman Becker highlighted ongoing innovation and growth despite macro softness in air travel, particularly as airline forecasts trend flat to down. Clear reaffirmed full-year FCF guidance of at least $310 million and guided Q3 revenue to $223-226 million (above consensus), with bookings expected to reach $253-258 million.

In a move atypical for growth-stage tech, the company declared a $0.125 per share quarterly dividend (1.62% yield), while continuing to return capital through buybacks. Analysts remain split – Goldman and Telsey reiterated bullish calls, while Wells Fargo stayed Underweight, citing decelerating metrics.

1

❖ Clearwater Analytics (CWAN) posted strong quarterly results, though with some caveats. See the “Under Review” section for details.

1

❖ ACM Research (ACMR) posted a mixed Q2 2025, with a strong EPS beat offset by a slight revenue shortfall. Revenue rose 6.4% year-over-year to $215.4 million, missing consensus of about $223 million, while non-GAAP EPS came in at $0.54, topping expectations by roughly 12%. Gross margin improved to 48.7%, exceeding the company’s 42–48% long-term target range, highlighting solid operational execution despite cost pressures. Shipments increased to $206 million from $157 million in Q1, driven by momentum in SPM, Tahoe, plating, and furnace tools, along with repeat orders for the upgraded Ultra C wb Wet Bench cleaning platform.

Management raised its long-term Mainland China revenue target from $1.5 billion to $2.5 billion, reflecting a higher estimated China WFE market size of $40 billion and increased market share goals of 60% in both cleaning and plating. The overall long-term company target also increased to $4 billion, while the rest-of-world target remains at $1.5 billion. ACM reiterated its full-year 2025 revenue guidance of $850–950 million (midpoint +15% YoY), signaling confidence in its demand pipeline despite the near-term revenue miss.

Net income was $36.8 million, down slightly from $37.5 million a year ago, as operating expenses climbed 38.8% to $63.4 million, reflecting higher investment in capacity and R&D. Cash and equivalents ended the quarter at $483.9 million, with net cash of $205.8 million, while inventory rose to $648.3 million as the company built components to support production and mitigate supply chain risk.

CEO Hui Wang underscored ACM’s strengthening position in advanced cleaning technologies and its readiness to meet AI-driven semiconductor demand. The Lingang R&D and production center is nearing completion, capable of supporting up to $3 billion in annual capacity, and U.S. expansion in Oregon is progressing toward a mid-2026 launch.

Shares dropped sharply on the revenue miss and softer shipment growth versus expectations, but analysts maintain a generally positive stance. Needham reiterated its Hold, while other coverage remains favorable, pointing to ACMR’s expanding product portfolio, higher China market share targets, and capacity growth as catalysts for recovery once near-term sentiment stabilizes.

1

❖ Backblaze (BLZE) saw its stock surge by over 24% on Thursday after the cloud storage and data backup company released a set of strong quarterly results.

BLZE posted a sharply positive Q2 2025 that delivered exactly the kind of turnaround patient investors hope for. Revenue grew 16% YoY to $36.3 million – beating consensus by about $0.9 million – and non-GAAP EPS came in at $0.01, a $0.06 beat versus expectations of –$0.05. The stock responded with a surge, as improved margins, AI-driven growth signals, and a strategic buyback ignited bullish momentum. The company has authorized a share repurchase program to purchase up to $10 million of shares of its common stock through August 1, 2026.

B2 Cloud Storage remained the growth engine – up 29% YoY from 23 % in Q1 – while computer backup rose 4%. Gross margin improved to 63 %, with adjusted gross profit hitting 79%, both higher than last year and reflecting operating leverage and cost discipline. The net loss narrowed to $7.1 million from $10.3 million, adjusted EBITDA more than doubled to $6.6 million, and the company posted its first non-GAAP quarterly profit at $0.8 million. Operational cash flow continued to improve, with H1 free cash flow loss reduced to –$6 million from –$11.6 million, and cash reserves at $50.5 million.

Product innovation supported the beat – with AI-powered Anomaly Alerts and the first six-figure B2 Overdrive customer signed just two months after launch. Up-market traction continued, with enterprise customers contributing over $50,000 in ARR growing 53% YoY. Management also authorized a $10 million cash-neutral share buyback, funded via employee stock option and ESPP proceeds, signaling confidence while managing dilution.

Wall Street took note – Needham raised its price target to $8.50 while reiterating Buy – and sentiment now leans toward further upside, with average analyst targets suggesting the potential for a significant re-rating over the next year.

This quarter’s sharp reversal from deep losses to modest gains reinforces the value of staying the course with well-positioned growth names – especially when operational momentum is building beneath the surface.

1

❖ Arlo Technologies (ARLO) delivered a record Q2 2025, comfortably surpassing expectations and reinforcing its strategic pivot toward high-margin subscription services. Revenue rose 10.2% YoY to $129.4 million, beating the Street’s $123.5 million estimate, while non-GAAP EPS of $0.17 topped the $0.15 forecast. The beat was powered by subscription and services revenue, which jumped 29.7% YoY to $78.2 million, now making up 60.4% of total sales. Annual recurring revenue (ARR) climbed 34.3% YoY to $315.7 million, with paid subscriptions up 218,000 sequentially to 5.1 million.

Margins expanded sharply – non-GAAP subscriptions and services gross margin reached a record 85%, up 850 basis points from last year – helping drive non-GAAP net income to $19 million and adjusted EBITDA to $18 million, a margin of 14% versus 6% a year ago. Management credited the launch of its AI-powered Arlo Secure 6 platform and disciplined cost control, alongside early wins from its channel refresh strategy. CEO Matthew McRae flagged the upcoming release of more than 100 new SKUs this fall and the recently announced ADT partnership as key growth levers, with the latter expected to materially lift subscription revenue from 2026 onward.

The company provided optimistic but grounded guidance. Q3 revenue is projected at $138 million at midpoint, above the $134.9 million estimate, while Q3 EPS is expected at $0.15 at midpoint, matching analyst forecasts. The full-year 2025 targets – revenue of $510-540 million and EPS of $0.56-0.66 – were reaffirmed, both essentially in line with consensus. The company also raised its 2025 service revenue target to above $310 million from ~$300 million previously, with ARR expected to end the year at $335 million, and service gross margins coming in above 85%. Arlo also broadened its long-term goals, aiming to reach 10 million paid accounts, $700 million in ARR, and an adjusted EBITDA margin above 25% by 2030.

The market’s reaction was swift – shares jumped more than 12% pre-market – supported by the existing “Strong Buy” consensus and an average price target implying nearly 30% upside even before these results. For long-term growth investors, ARLO’s quarter underscores how steady execution and a high-margin subscription base can drive resilience, even in a competitive consumer tech landscape.

1

1

Under Review

❖ We are keeping Clearwater Analytics (CWAN) under review, maintaining a “hold-with-vigilance” strategy.

This decision follows its Q2 2025 earnings and sharp post-report selloff. Despite strong operational results, the stock has now fallen over 30% from its February highs – more than 10% of that on earnings day alone – indicating technical breakdowns and market skepticism are outweighing fundamentals for now.

Revenue rose 70.4% year-over-year to $181.9 million, beating estimates by $7.8 million. Non-GAAP EPS of $0.12 matched expectations, while adjusted EBITDA rose 74% to $58.3 million. Annualized recurring revenue climbed 83% to $783.5 million, and gross revenue retention held steady at 98% – all signs of healthy customer growth and integration execution. Non-GAAP gross margin remains solid at 77.4%. The company also reaffirmed a strong Q3 outlook, projecting 75-76% YoY revenue growth.

However, the GAAP net loss widened to $24.2 million due to acquisition-related costs, and free cash flow growth slowed to just 4% YoY. Total debt ballooned to $878 million as Clearwater integrated Enfusion, Beacon, and BISTRO – a capital-intensive strategy that is beginning to test investor patience, particularly in a high-rate environment. Sentiment may have been further dented by the absence of an upward revision to full-year margin or FCF guidance despite strong top-line beats.

Meanwhile, CWAN’s business momentum remains positive, with several high-profile customer wins and partnerships – notably with Bloomberg, which will integrate Clearwater’s accounting platform into its enterprise investment solutions – tilting our sentiment toward continuing to hold the stock in the Portfolio. The latest results validate its acquisition and integration strategy, delivering growth and margin expansion even amid complexity. Its infrastructure platform, expanding institutional partnerships, and strong retention metrics preserve upside potential.

Analysts remain bullish overall – Oppenheimer reiterated a Buy with a $36 target, and Loop Capital maintained its Buy with a reduced $31 target – but some are tempering expectations around synergy timelines. The bullish case still hinges on Clearwater’s ability to scale acquired assets from 13% to 20% revenue growth, improve margins, and convert debt-fueled expansion into durable SaaS profitability. While these deals strengthen Clearwater’s position as a front-to-back investment operations platform, the path to earnings leverage is under closer scrutiny.

For now, we remain cautious but not bearish. Clearwater is executing well on integration and client expansion, but with the market in wait-and-see mode, we prefer to stay on the sidelines. The stock remains under review until we see renewed traction on cash flow, debt reduction, or a reacceleration in valuation momentum.

1

1

1

This Week’s Top Growth Pick: Paymentus Holdings (PAY)

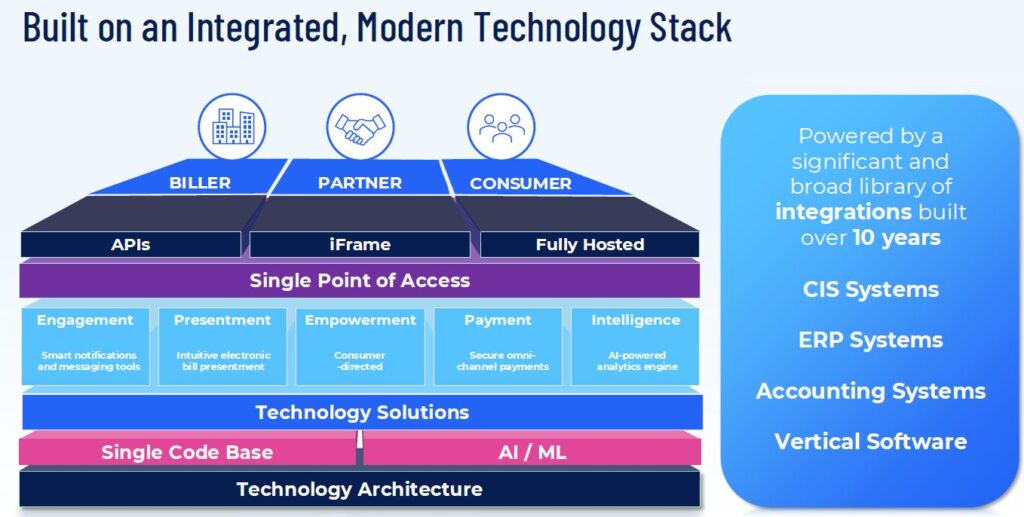

Paymentus Holdings, Inc. is a cloud-based billing and payments technology provider serving billers, financial institutions, and consumers across North America. Its platform enables real-time electronic bill presentment, payments, and customer communications through multiple channels including web, mobile, text, voice, and kiosk. Designed to streamline the full billing lifecycle, Paymentus integrates with a wide range of enterprise systems and payment methods while supporting clients in sectors such as utilities, healthcare, insurance, and government. The company emphasizes scalability, flexibility, and user experience, allowing billers to accelerate digital adoption and improve payment efficiency. With a unified architecture and broad distribution partnerships, Paymentus plays a key role in modernizing bill payment infrastructure and expanding consumer access to financial services across traditional and embedded banking environments.

Source: Paymentus Investor Presentation, May 2025

1

Bill Me Forward

Paymentus Holdings began in 2004 with a focus on digitizing the fragmented bill payment process for utilities, insurers, public agencies, and other recurring billing organizations. Over the past five years, the company has evolved into a full-stack, real-time billing and payments platform used by over 2,000 billers across North America. It went public in May 2021, marking a key inflection point as it expanded both product capabilities and distribution reach.

One of the most significant developments during that period was PAY’s embedded bill pay distribution agreement with JPMorgan Chase, announced in 2021. This long-term partnership gave the company direct access to millions of banking customers through Chase’s digital channels. The relationship remains active and accretive, with Chase continuing to onboard new billers onto the platform through mid-2025.

Alongside this, Paymentus has broadened its financial institution footprint through integrations with platforms like Banno (Jack Henry), Alkami, and Q2 – allowing banks and credit unions to offer its billing and payment features directly within digital banking interfaces. These partnerships have become a key channel for acquiring new biller relationships and deepening consumer engagement.

On the infrastructure side, Paymentus has steadily invested in scalable hybrid cloud and private data center deployments. Rather than relying on third-party hyperscalers for core processing, the company has emphasized control, security, and cost efficiency through its own managed environments. This architecture underpins its ability to deliver real-time, multi-channel payments with high reliability – a foundational element of its value proposition.

The past few years have also seen expanded use cases beyond core bill pay, including disbursements, payment reminders, mobile wallet support, and consumer messaging. The company has rolled out these features incrementally across its client base, driving up platform revenue per biller without compromising modularity.

PAY’s growth trajectory reflects a consistent strategy: expand through embedded channels, innovate within the platform’s boundaries, and scale through performance-first infrastructure. With demand for digital billing accelerating across both enterprise and public sector clients, the company has steadily captured share in a legacy-dominated market – gaining momentum without sacrificing operational discipline.

Source: Paymentus Investor Presentation, May 2025

1

Essentially Paid

Paymentus operates a cloud-native platform that digitizes the most reliable corner of consumer finance: non-discretionary bill payments. Utility bills, insurance premiums, healthcare copays and government fees don’t stop when the economy slows – they get paid. These are inelastic, recurring obligations with consistent transaction volumes, and they form the bedrock of PAY’s model.

What sets Paymentus apart is its ability to bring this traditionally offline, fragmented category into the digital age through its end-to-end billing, presentment and payments platform. It gives billers a modern interface to engage consumers across channels – web, mobile, text, IVR and even in-store retail – while automating everything from reminders to reconciliations. The company’s cloud-native architecture allows it to scale rapidly, handle high transaction volumes and deploy updates seamlessly – a critical advantage in a sector where agility is key.

The company earns nearly all of its revenue through a transaction-based, SaaS-like model with strong recurring characteristics. Roughly 93% of revenue comes from Platform and Usage Fees, which scale with transaction volume and adoption. The rest (7%) comes from Customer Support and Other Services, such as onboarding and call center support.

At the center of it all is the Instant Payment Network (IPN) – a unified payment layer that integrates digital wallets like Apple Pay and PayPal, real-time ACH rails and embedded banking platforms. IPN routes billions in payment volume with high reliability, enabling instant account-to-account transfers and dramatically reducing friction for both billers and consumers. Features like AI-powered chatbots and the X3 analytics engine further enhance its stickiness – cutting service costs and driving operational insights. Paymentus is deploying Agentic AI to automate workflows, reduce manual interventions and extract actionable insights for clients. This not only lowers costs but also enhances client retention.

By anchoring itself to essential services, PAY is insulated from cyclical swings in consumer spending. This gives it a high degree of volume predictability – a rare advantage in fintech. The company’s ecosystem approach expands its total addressable market beyond bill pay software. By enabling in-store payments at Walmart and CVS, Paymentus accesses unbanked and underbanked populations who transact in cash. Collaborations with Citizens Financial Group, Accelerated Innovations and digital banking providers like Alkami and Jack Henry’s Banno have widened its reach within regulated industries and banking.

Paymentus estimates its U.S. addressable market at $1.5 trillion in real-time bill payments. Despite serving over 2,000 billers, its penetration remains in the low single digits, suggesting meaningful upside through share gains and deeper integrations. The company has also disclosed a $500 million ARR backlog from contracts not yet fully ramped – a clear indicator of latent growth built into its channel distribution.

As demand shifts toward embedded, omni-access billing experiences, PAY is increasingly positioned as both the infrastructure and the interface – offering scale, real-time reach and platform economics in a sector historically dominated by slow, fragmented incumbents. In a space often overlooked by flashier fintechs, Paymentus is building the rails for a critical, high-frequency and highly monetizable segment of financial infrastructure – one invoice at a time.

Source: Paymentus Investor Presentation, May 2025

1

Processing the Future

Paymentus delivered another strong quarter in Q2 2025, with results exceeding both analyst expectations and internal forecasts. Revenue rose 41.9% year-over-year to $280.1 million, driven by broad-based growth across biller count and transaction volume. The company processed 175.8 million transactions in the quarter – up 25.2% from the prior year – with average revenue per transaction rising from $1.41 to $1.59.

PAY also reported an incremental adjusted EBITDA margin of 53.8% – a signal of strong operating leverage and cost discipline, particularly as volume discounts were offset by efficient onboarding of large clients and improvements in product mix. Contribution profit rose 22.3% to $93.5 million, while adjusted EBITDA surged to $95 million, reflecting a 33.9% margin – the highest in company history.

Importantly, this performance marked the first time Paymentus has exceeded the Rule of 40, a SaaS benchmark that combines revenue growth and EBITDA margin. With 41.9% top-line growth and a 33.9% EBITDA margin, PAY posted a combined score of 75.8 – underscoring the scalability and efficiency of its transaction-driven model.

Earnings continued to scale in parallel. GAAP net income reached $14.7 million, up from $9.4 million in the prior year – a 56% YoY increase – with GAAP EPS rising to $0.11 from $0.07. This marked the sixth consecutive Q2 of GAAP profitability, highlighting the durability of PAY’s margin structure. On a non-GAAP basis, net income increased to $19.3 million, with EPS of $0.15 versus $0.10 last year – beating Street expectations by a wide margin. In fact, the company’s non-GAAP EPS has surpassed analyst consensus in every quarter since Q4 2022.

Paymentus ended Q2 with $278.6 million in cash and equivalents. Operating cash flow reached $31.5 million for the quarter, while free cash flow rose to $21.3 million – up sharply from just $6.3 million in the year-ago period – reflecting strong discipline even as enterprise onboarding ramps up. The company ended the quarter with no debt and a sizable cash buffer, thanks in part to minimal capex and capital-light scaling.

Looking ahead, management raised its full-year 2025 guidance. Revenue is now expected to reach $1.123-1.132 billion, implying 35-36% growth over 2024. Contribution profit is forecast between $369-373 million, while adjusted EBITDA is projected at $123-127 million – both up meaningfully from prior targets. Analyst consensus sits at the lower end of that range, suggesting upside if current momentum holds.

Supporting this guidance is a growing backlog of over $500 million in annual recurring revenue potential, driven largely by large enterprise wins in utilities, government and telecom. These accounts are high-volume, low-churn and typically generate multi-year engagement – providing Paymentus with strong visibility into 2025 and 2026. As demand for real-time payments and omnichannel billing intensifies, this backlog gives PAY a long runway for compounding growth across both new and existing channels – proving that financial infrastructure built for reliability can also deliver accelerating returns.

Source: Paymentus Q2 2025 Earnings Presentation

1

PAY It Forward

Paymentus’ consistent revenue and EPS beats, coupled with its strong fundamentals and scalable business model, have driven stock outperformance relative to a broad set of peers – from mid-caps to large players, spanning SaaS-native bill pay automation providers, merchant-facing platforms, and enterprise fintech infrastructure firms.

PAY has gained more than 80% over the past 12 months. Despite that, consensus still calls for an additional upside of ~19% – which may well rise as analysts reassess the recent earnings report and raise their price targets. Paymentus’ stock coverage is not extensive, and analysts often scramble to revise their forecasts following each quarterly beat.

Meanwhile, valuation remains reasonable, even if not cheap. The stock currently trades more than 15% below its 52-week high. While PAY’s non-GAAP P/E and EV/EBITDA ratios (TTM and forward), as well as TTM Price/Cash Flow, are above those of many peers, the premium is justified by a stronger balance sheet, consistent profitability gains, and superior growth rates across revenue, EBITDA, and EPS – both historical and forecasted.

Moreover, despite robust revenue growth and healthy gross margins, Paymentus trades near the midpoint of peer valuation multiples on a TTM and forward EV/Sales basis – suggesting a balanced valuation per dollar of revenue. Its Forward PEG ratio of approximately 1.1 implies that the current price reflects its high-growth profile without excessive optimism.

While Paymentus hasn’t initiated any buybacks, its shareholders haven’t been diluted. Insider ownership remains high, and institutional ownership provides additional stability. Notably, there has been no recent insider selling. On the contrary, company insiders – including board members and executives – have increased their stakes, with founder and CEO Dushyant Sharma boosting his holdings to approximately 15.5% of the float, a clear vote of confidence in the company’s long-term trajectory.

With operational leverage kicking in, backlog visibility extending into 2026, and institutional confidence high, Paymentus appears well-positioned to compound gains – even from elevated levels. As the market gradually catches up to the company’s execution and outlook, PAY still offers meaningful upside for growth-focused investors willing to ride the next leg of digital bill pay adoption.

1

To Sum It All Up

Paymentus powers a modern billing and payments platform built for scale, speed, and reliability. Anchored in non-discretionary bill payments, it serves essential sectors like utilities, healthcare, insurance, and government – markets defined by high volume, low churn, and recession resistance. Its cloud-native architecture and Instant Payment Network enable seamless, omni-channel payment experiences while driving efficiency and cost savings for clients. Paymentus stands apart from legacy processors and upstart fintechs by combining enterprise-grade infrastructure with a transaction-based SaaS model that grows as usage scales. With rising adoption across large enterprises, growing channel partnerships, and a massive addressable market still largely untapped, Paymentus offers a unique growth story at the intersection of financial infrastructure, real-time payments, and digital automation.

1

1

Smart Growth Portfolio

|

1

1

Disclaimer

The information contained in this article represents the views and opinions of the writer only, and not the views or opinions of TipRanks or its affiliates and should be considered for informational purposes only. TipRanks makes no warranties about the completeness, accuracy, or reliability of such information. Nothing in this article should be taken as a recommendation or solicitation to purchase or sell securities. Nothing in the article constitutes legal, professional, investment and/or financial advice and/or takes into account the specific needs and/or requirements of an individual, nor does any information in the article constitute a comprehensive or complete statement of the matters or subject discussed therein. TipRanks and its affiliates disclaim all liability or responsibility with respect to the content of the article, and any action taken upon the information in the article is at your own and sole risk. The link to this article does not constitute an endorsement or recommendation by TipRanks or its affiliates. Past performance is not indicative of future results, prices, or performance.