TipRanks Smart Growth Portfolio #30: Control Shift

Dear Investors,

Welcome to the 30th edition of the Smart Growth Portfolio and Newsletter.

1

1

Portfolio Updates

❖❖❖ We’re selling Clearwater Analytics (CWAN) from the Growth Portfolio.

The fundamentals are not the issue – execution has been strong, retention is high, margins are healthy, and management just put a $100 million buyback in place – but the tape keeps rejecting the story. Even modestly positive headlines have been sold, which tells you sentiment is entrenched on the downside. After weeks of thin newsflow, the stock continues to drift lower. That’s a falling-knife setup, not a base.

Our thesis under review hinged on two things materializing in the near term: proof that the Enfusion/Beacon/BISTRO integration would translate into visible operating leverage, and a sentiment turn as investors credited CWAN’s platform expansion. Instead, the market remains fixated on leverage and acquisition risk, and the post-print reaction reinforced that skepticism. Analyst support is strong – but largely irrelevant to price discovery right now. When a stock sells off on good news and shrugs off buyback support, you have to acknowledge the market’s signal.

Could CWAN be a profitable long-term investment? Absolutely. The platform logic is sound, the client roster is real, and the private-credit tooling is timely. But capital is finite, and drawdowns compound opportunity cost. We’ve seen other holdings with catalysts align and rip back from significant paper losses; CWAN hasn’t shown that inflection. Relying on sentiment to turn without a clear catalyst risks deeper losses and wasted capital.

We’re exiting now and preserving capital for higher-conviction ideas with nearer-dated catalysts. If CWAN turns, we can buy it back – it will take a lot to make it not cheap, so there should be time to re-enter on strength rather than hope. What would get us back in: a clean, beat-and-raise quarter; tangible integration KPIs that map to ARR expansion and operating margin accretion; evidence of deleveraging from organic cash generation; and price stability that holds gains after good news. Until then, the asymmetry favors avoiding further downside while keeping CWAN on the watchlist for a sustained reversal.

1

1

Portfolio News

❖ Micron (MU) reported a spectacular quarter, closing an exceptional fiscal year – with beats on consensus estimates underscoring how AI demand is reshaping the memory market. FQ4 revenue surged 46% year-over-year, and non-GAAP EPS of $3.03 topped expectations by a wide margin, marking a seventh straight quarter of triple-digit earnings growth.

DRAM revenue – nearly 80% of total – reached $9 billion, up 69% YoY, more than offsetting a 5% decline in NAND revenue. Gross margin expanded to 45.7%, and operating cash flow jumped to $5.73 billion, reflecting favorable pricing and cost discipline. Explosive AI data center demand was the key driver, with HBM sales nearing $2 billion in FQ4 alone. Data center revenue accounted for 40% of the quarter’s total, highlighting the impact of the AI infrastructure boom on Micron’s business mix and long-term outlook.

Fiscal 2025 revenue rose 49% YoY to a record $37.4 billion, with gross margin up 17 percentage points to 41%. DRAM revenue climbed 62% YoY, while NAND posted 18% growth despite the Q4 dip. The data center segment delivered record results, making up 56% of total company revenue at a 52% gross margin. Non-GAAP net income was $9.47 billion, or $8.29 per share – an astonishing 538% increase from the prior year.

Micron issued a bullish outlook for both FQ1 2026 and the full fiscal year. For the current quarter, it projects revenue of $12.5 billion, EPS of $3.75, and gross margins around 51.5% at the midpoint. Margins above 50% for the first time since 2018 signal strong pricing power as supply tightens – and all midpoint outlooks came in well ahead of Street estimates.

Guidance for fiscal 2026 is similarly upbeat. CEO Sanjay Mehrotra emphasized Micron’s unique position as the only U.S.-based memory manufacturer, highlighting leadership in HBM, 1-gamma DRAM, and G9 NAND. Full-year 2026 expectations call for significantly higher free cash flow and record revenue growth. Management also pointed to NAND strength from hyperscaler demand, tightening DRAM conditions, and an exit from managed NAND for smartphones to sharpen focus on higher-ROI markets like data center SSDs. HBM momentum is central – the HBM4 line is nearly sold out for 2026 – and surging AI demand is driving higher capex plans, up to ~$18 billion from $13.8 billion in 2025, concentrated on DRAM and HBM expansion.

Analyst reaction was near-exuberant, with roughly two dozen price-target upgrades pushing the average target about 23% above current levels – even with MU already up more than 85% year-to-date. Still, the stock fell over 6% after earnings, echoing prior quarters. Much of this looks like “sell the news,” amplified by recent tech volatility, as Micron’s August 11 pre-announcement fueled a 35% rally into the print. Short-term volatility aside, Micron’s leverage to the data center cycle, strong execution, and leadership in HBM – combined with robust fundamentals and a still-reasonable valuation – keep it well-positioned for further gains.

1

1

1

This Week’s Top Growth Pick: AvePoint (AVPT)

AvePoint is a cloud-centric software company focused on data management, security, and governance across major collaboration ecosystems like Microsoft 365, Google Workspace, and Salesforce. Its flagship Confidence Platform is designed to handle migration, backup, access control, and compliance under one framework – reducing the need for multiple point solutions. Through its SaaS platform, AvePoint has evolved into a key enabler for organizations navigating digital transformation, cloud migration, and AI-driven workplace challenges. By embedding governance and resilience into everyday collaboration, AvePoint helps enterprises adapt to rapid shifts in how work gets done – from hybrid office demands to growing compliance pressures. Its role sits at the intersection of productivity and protection, positioning the company as an essential layer in the modern digital workplace.

Source: AvePoint company website

1

Backup History

AvePoint began in the early 2000s as a specialist in Microsoft SharePoint migration and management, gradually building credibility in governance, backup, and compliance. The company’s real transformation, however, has come over the past five years, as it shifted decisively to SaaS, embraced AI, and expanded its reach through acquisitions and partnerships.

The turning point arrived in 2021, when AvePoint went public via a SPAC merger with Apex Technology and listed on Nasdaq under the ticker AVPT. The listing provided capital to accelerate research and development, strengthen go-to-market channels, and expand globally. Building on this momentum, AvePoint pursued a string of acquisitions in 2022 and 2023, including Essential Co., Combined Knowledge, i-Access Solutions, and tyGraph. These deals broadened its analytics, training, and regional coverage, helping position the company as more than a Microsoft add-on vendor. In early 2025, AvePoint added Ydentic, a Netherlands-based MSP automation platform, integrating service management and automation capabilities into its Elements platform to drive growth among managed service providers.

Alongside M&A, AvePoint invested heavily in internal innovation. It extended its Confidence Platform into Microsoft’s Power Platform, added new layers of AI-driven information lifecycle management, and embedded machine learning into content classification and governance tools. These steps shifted its focus from reactive protection to proactive optimization of collaboration data. By adopting the same AI tools internally, such as Microsoft Copilot, AvePoint also demonstrated how its own workforce could serve as a proving ground for these capabilities.

Strategic partnerships reinforced this trajectory. AvePoint remained tightly aligned with Microsoft, becoming an exclusive Content AI partner in 2023 while continuing to integrate with Microsoft 365, Teams, and Purview. At the same time, it expanded coverage across Google Workspace and Salesforce, ensuring its governance and protection tools were relevant in multi-cloud environments.

Capital backing has underpinned this expansion. In 2023, the company secured an anchor investment from 65 Equity Partners, the growth fund linked to Temasek (Singapore’s sovereign wealth fund), which provided resources for scaling and helped pave the way for its dual listing on the Singapore Exchange. That listing was completed in September 2025, making AvePoint the first B2B SaaS company to trade on both Nasdaq and SGX – a step designed to deepen liquidity and strengthen its profile in Asian markets. With these milestones, AVPT has laid the groundwork for the next stage of its story – one defined by scaling its SaaS platform, broadening its customer base, and capturing a larger share of the digital workplace transformation.

Source: AvePoint Q2 2025 Investor Presentation

1

Cloud Formation

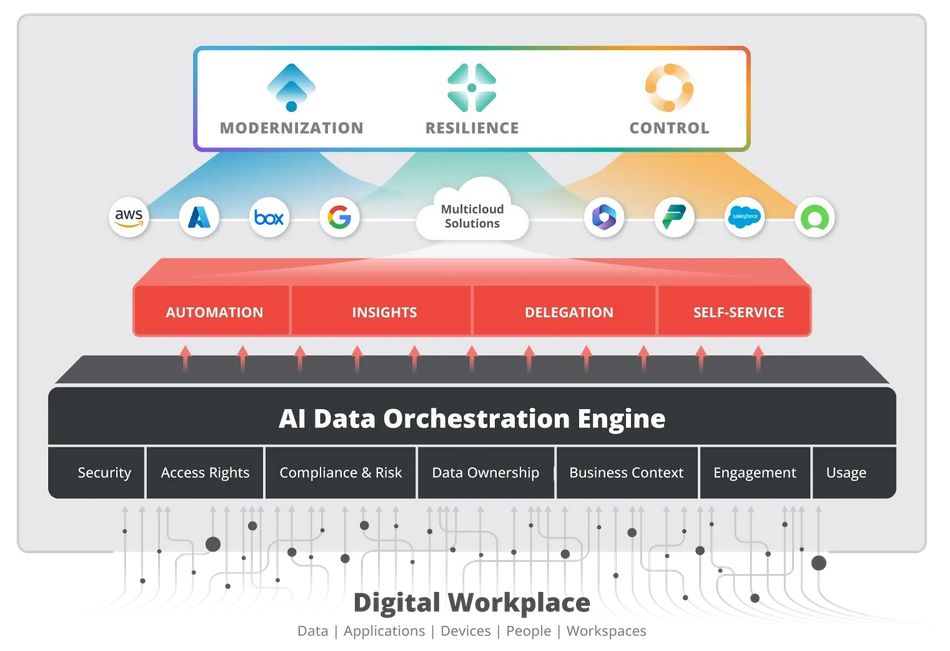

AvePoint is a SaaS-driven business built on subscriptions to its Confidence Platform, which delivers data protection, governance, and modernization tools for collaboration ecosystems. SaaS contributes 75% of total revenue and recurring contracts overall account for 87% – a model that provides high visibility and consistent growth while reducing reliance on one-off service engagements. Professional services exist mainly to accelerate adoption, not to drive scale.

The platform is structured around three suites. Resilience, which includes cloud backup and disaster recovery, is the largest segment and represents nearly two-thirds of annual recurring revenue. Control, focused on governance and compliance automation, contributes close to one-third. Modernization, covering migration and lifecycle management, is smaller but strategically important as it brings new customers onto the platform and feeds cross-sell opportunities. This mix illustrates how AvePoint monetizes both the urgent needs of enterprises – protecting critical data and ensuring regulatory compliance – and the longer-term shift toward optimizing how cloud environments are managed.

What distinguishes AVPT is the breadth and integration of these functions. Many competitors like Veeam or Druva remain largely focused on backup and recovery. Microsoft Purview offers compliance controls but is limited to the Microsoft stack. Against this backdrop, AvePoint stands out as it not only embeds deeply in Microsoft 365, Teams, and Power Platform but has also extended into Google Workspace and Salesforce applications such as Sales Cloud and Service Cloud, with support now expanding in AWS environments. This creates a broader governance layer that customers can use across clouds rather than stitching together multiple point solutions. That integration is particularly important for enterprises preparing to deploy AI assistants like Copilot, where ensuring data security and policy enforcement across collaboration platforms is non-negotiable.

Source: AvePoint Q2 2025 Investor Presentation

Scale is amplified by AvePoint’s global partner network. More than 5,000 managed service providers, value-added resellers, and system integrators distribute and implement the platform, particularly in the mid-market and SMB segments. This channel-centric go-to-market model allows AVPT to grow efficiently – expanding reach without proportional increases in service costs – and often accounts for the majority of sales mix alongside direct enterprise deals.

Growth also benefits from external tailwinds. The One Big Beautiful Bill (OBBB) fiscal package restored immediate R&D expensing and extended bonus depreciation in the U.S., improving cash flexibility for software firms investing heavily in product development. For AvePoint, this makes it easier to sustain rapid innovation in AI-driven governance and security at scale. At the same time, federal programs are now channeling more resources into cloud adoption and cybersecurity for government agencies, reinforcing demand in one of the company’s most stable verticals.

The market backdrop provides additional runway. Industry estimates put AvePoint’s long-term addressable market for data security, governance, and modernization at roughly $140 billion by 2028, expanding at an annual compound rate in the mid-teens. With only a small slice of the market today, the company has substantial scope to increase penetration.

Source: AvePoint Q2 2025 Investor Presentation

1

Cash Points

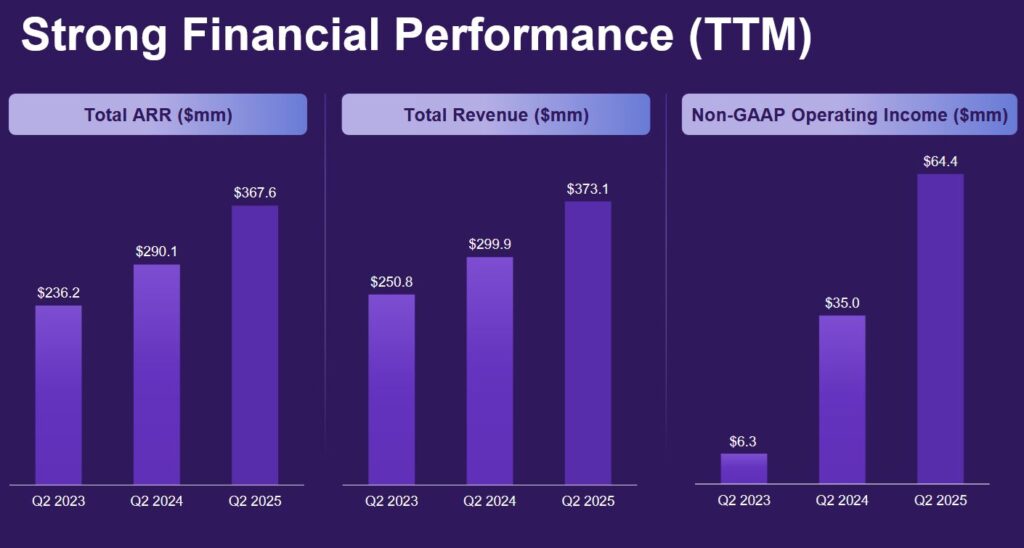

AvePoint entered the second half of 2025 with clear financial momentum, delivering a record quarter that surpassed internal goals and largely met analyst expectations. Revenue in Q2 rose 31% year-over-year to $102 million, the first time the company has crossed the $100 million mark. The top line was powered by SaaS subscriptions, which grew 44% to $77.3 million and represented 76% of total revenue, underscoring the company’s continued transition to a higher-margin recurring model. Annual recurring revenue reached $367.6 million, up 27% from the prior year, with net new ARR of $22.1 million – the largest quarterly addition in its history – reflecting strength across North America, EMEA, and especially APAC.

Profitability also moved in the right direction. Non-GAAP operating income climbed to $18.8 million, or an 18.4% margin, expanding more than 700 basis points from the prior year. The gains were driven by improved sales efficiency and rising channel contribution, which allowed growth without proportional increases in operating costs. Gross margin came under some pressure, easing to 74.8% from 76.2% a year ago due to a higher mix of lower-margin services, but this was more than offset by the leverage evident in operating results.

Non-GAAP EPS flipped from a $0.01 loss in Q2 2024 to a $0.06 profit in Q2 2025, a sharp improvement and another quarter of outperformance. AVPT has beaten analyst consensus on earnings in 12 of 17 quarters since going public, while exceeding revenue expectations in every quarter for the past two years. On a GAAP basis AVPT remains unprofitable, though losses narrowed, and the company has now posted several quarters of consistent non-GAAP profitability – a marker of its progress toward sustained GAAP profitability in the medium term.

Cash generation showed some near-term pressure. Operating cash flow for the first half of 2025 was $20.8 million, down from $23.9 million in the prior-year period, reflecting heavier investment in R&D and go-to-market initiatives as well as working-capital timing. Free cash flow also declined modestly but remained positive, underscoring that AVPT is reinvesting aggressively while maintaining discipline. The balance sheet is solid, with $236 million in cash and equivalents at quarter-end and no debt, providing ample liquidity and flexibility to pursue growth.

Looking ahead, management raised full-year guidance, projecting revenue of $406.6-410.6 million, up 23-24% year-over-year, and ARR of $412.8-418.8 million, up 26-28%. Non-GAAP operating income is expected to reach $68.3-70.8 million, translating into margins of 16.8-17.2% for the year. Analyst consensus sits close to the midpoint of these ranges, suggesting guidance is realistic yet still leaves room for upside if momentum in SaaS adoption and partner-driven expansion holds through year-end. The long-term target of $1 billion in ARR by 2029 remains intact, with current performance demonstrating that AvePoint is building the scale and efficiency to make that ambition credible.

Source: AvePoint Q2 2025 Investor Presentation

1

Backup Metrics

AvePoint’s peer group includes a diverse set of data management and protection firms, spanning stages from small-cap growth to scaled incumbents. The closest comps are Varonis, a SaaS-transitioning specialist in data governance and protection; Rubrik, a high-growth player in cloud data protection and ransomware recovery; Commvault, an established incumbent in enterprise backup and protection; and OpenText, a diversified enterprise information management provider with a more mature profile.

The past year has been volatile for software firms, with the AI advance initially driving skepticism about the industry’s future viability. As the year progressed, sentiment shifted more toward macro and company-specific factors, with investors largely favoring either stable, profitable firms or those making headlines (such as Rubrik’s partnership with CrowdStrike and Varonis’ strong push into cybersecurity, a hot topic lately).

While AvePoint’s profitability metrics are improving faster than many of its peers, its smaller size, limited headline coverage, and absence of splashy deals have weighed on the stock. Despite strong Q2 earnings, a dip in margins and uncertainty in public-sector contracts pressured performance, leading to underperformance since early August. Still, with all the volatility, AVPT is up almost 30% in the past year – nearly double the S&P 500. Its consistently strong revenue growth and a clear path to profitability support an optimistic outlook for the stock, which is also reflected in the Street’s “Strong Buy” consensus and an average price target that implies more than 40% upside.

Meanwhile, AvePoint’s valuations remain moderate relative to its revenue growth rates – both actual and forecasted – which are second only to Rubrik among peers. Its trailing and forward EBITDA growth also surpass all of them by a large margin. Beyond that, AVPT’s profitability metrics, including EBITDA margin, ROE, ROA, and net income margin, are the strongest among the high-growth subset of peers, with a premium above lower-growth incumbents clearly justified by its expansion trajectory.

Against this backdrop, valuation metrics – including trailing and forward EV/Sales, Price/Sales, and forward non-GAAP P/E – look moderate compared to higher-growth peers. AVPT’s forward EV/EBITDA multiple is also lower than Varonis (Rubrik remains unprofitable), underscoring stronger cash-generating ability.

On top of this, AvePoint also offers share enhancement through buybacks. In February 2025, the company increased its equity repurchase authorization to $150 million and extended the plan by three years. Over the first half of 2025 alone, it retired ~$19 million worth of stock, equal to about 0.6% of shares outstanding.

AvePoint is growing fast, scaling profitably, and buying back its own stock – and with valuations still moderate compared to high-growth peers, it stands out as one of the more interesting stories in data management right now.

1

To Sum It All Up

AvePoint offers a growth investment case built on governance, resilience, and scale. The company sits at the center of enterprise demand for secure collaboration – protecting and managing data as organizations expand across multi-cloud and AI environments. Its Confidence Platform turns governance into a recurring SaaS model, with expanding suites that deepen retention and drive cross-sell. Execution has been steady, with consistent growth, rising profitability, and disciplined reinvestment. Yet the stock trades at moderate valuations compared with peers despite one of the strongest growth profiles in the group. With secular tailwinds in compliance and AI-ready data management, AvePoint is positioned as a durable compounder the market hasn’t fully recognized.

1

1

Smart Growth Portfolio

|

1

1

Disclaimer

The information contained in this article represents the views and opinions of the writer only, and not the views or opinions of TipRanks or its affiliates and should be considered for informational purposes only. TipRanks makes no warranties about the completeness, accuracy, or reliability of such information. Nothing in this article should be taken as a recommendation or solicitation to purchase or sell securities. Nothing in the article constitutes legal, professional, investment and/or financial advice and/or takes into account the specific needs and/or requirements of an individual, nor does any information in the article constitute a comprehensive or complete statement of the matters or subject discussed therein. TipRanks and its affiliates disclaim all liability or responsibility with respect to the content of the article, and any action taken upon the information in the article is at your own and sole risk. The link to this article does not constitute an endorsement or recommendation by TipRanks or its affiliates. Past performance is not indicative of future results, prices, or performance.