TipRanks Smart Growth Portfolio #43: Proof of Control

Dear Investors,

Dear Investors,

Welcome to the 43rd edition of the Smart Growth Portfolio and Newsletter, where we spotlight a government-embedded cybersecurity and identity compounder. But first, some news and updates.

1

1

Portfolio News

❖ Micron (MU) saw its shares spike to a record high on news that the U.S. administration has decided to delay semiconductor tariffs on China for at least 18 months to support a fragile trade truce. This comes despite the year-long investigation into Chinese chip-industry practices, which concluded that unfair government support – aimed at global dominance and increasing U.S. reliance on Chinese supplies – poses significant national security risks.

The decision to delay tariffs is a net positive for Micron in the short term, as it reduces immediate risks of supply chain disruptions or Chinese retaliation. While tariffs could eventually protect MU from Chinese government-subsidized competition, they could also harm it through counter measures.

Micron has actively reduced its China-based revenue over the past several years, with direct sales exposure now estimated at roughly 10-15%. However, an abrupt tariff hike could have spiked costs and constrained the supply of Chinese-sourced components.

Moreover, MU – a flagship domestic memory producer carrying a significant “Made in U.S.A.” symbolism – has seen its fair share of China’s “retaliation” practices over the years, and the current U.S. decision negates the risk of another strike.

The 18-month buffer also provides time for Micron to continue diversifying its supply chains and investing in domestic production. In June, the company announced a massive $200 billion U.S. investment plan, which covers the full spectrum of memory production while emphasizing HBM manufacturing. Micron’s strategy is to bring the entire HBM manufacturing process – from chip fabrication to the highly complex advanced packaging stage – onto U.S. soil, and the period of stability following the prolonged tariff truce gives the company the breathing space it needs to further these plans.

1

❖ The decision to delay new tariffs on Chinese semiconductor imports until at least June 2027 is also positive for ACM Research (ACMR), Applied Digital (APLD), and Backblaze (BLZE).

ACMR is a U.S. firm, but most of its operations are performed through its Shanghai subsidiary, with the lion’s share of revenue coming from sales to Chinese chip foundries. A sudden tariff hike could both freeze ACMR customers’ capex and lead to Beijing favoring purely domestic toolmakers over ACMR – a major risk given the company’s deep integration into the Chinese ecosystem.

For Applied Digital, the impact is primarily about capex costs. As the company aggressively expands its HPC and AI data centers, the buildout requires a massive amount of power management chips, networking hardware, and basic microcontrollers – many of which are currently sourced from China. The tariff delay prevents an immediate 10-25% spike in the cost of these legacy components, keeping construction budgets for 2026 intact.

Backblaze feels the impact through the cost of hardware like HDDs and SSDs, which it uses to provide cloud storage. Many components in these drives – such as controllers and bridge chips – are manufactured in Chinese foundries, meaning the tariff freeze helps BLZE maintain competitive storage pricing during a period where hardware costs are already trending upward.

1

1

1

This Week’s Top Growth Pick: Telos Corporation (TLS)

Telos Corporation is a cybersecurity and compliance-focused software company helping organizations protect sensitive systems, data, and digital identities in high-stakes environments. Its platforms are designed to secure critical infrastructure, manage cyber risk, and support complex regulatory and accreditation requirements across government and enterprise customers. Operating at the intersection of cloud security, identity management, and continuous compliance, Telos emphasizes prevention, visibility, and resilience rather than reactive defense. The company’s technology is built for environments where trust, uptime, and verification are non-negotiable – from national security systems to regulated commercial networks. As cybersecurity shifts toward continuous monitoring and zero-trust architectures, Telos positions itself as an enabler of secure digital operations, translating policy and risk frameworks into operational, software-driven safeguards.

Source: Telos Corporation Website

1

Automated Trust Machine

Telos traces its roots back more than five decades as a trusted provider of mission-critical technology to U.S. federal agencies, but its modern identity has been shaped largely over the past five years. A pivotal moment came in late 2020, when the company entered public markets, giving it the capital and visibility to accelerate a long-planned shift away from legacy IT services toward software-driven cybersecurity and compliance platforms. That transition was much more than simply a cosmetic change – it marked a deliberate narrowing of focus toward areas where Telos had long-standing credibility: securing high-impact systems under the most demanding regulatory regimes.

The strategic reset gained momentum as Telos doubled down on its proprietary software portfolio, particularly its continuous compliance and cloud security offerings. The company steadily evolved its flagship product Xacta from a compliance documentation tool into a broader platform designed to automate authorization, monitoring, and risk management across complex environments. This positioned Telos squarely within the federal government’s push toward continuous authorization and zero-trust frameworks, rather than static, point-in-time certification models.

A defining transformation occurred in 2023, when TLS divested its legacy identity and access management services business, simplifying the company’s structure and sharpening its focus on scalable cybersecurity platforms. The divestiture did not represent a complete exit from identity altogether, but rather removed lower-scalability consulting-style offerings, allowing management to concentrate resources on software-driven security, compliance automation, and large-scale, programmatic identity operations under Telos ID.1 This shift reinforced a long-term growth narrative centered on platform depth and repeatable program revenue, rather than fragmented service delivery.

Partnerships have played a central role in this evolution. Telos deepened its collaboration with hyperscalers by aligning its flagship Xacta platform with AWS GovCloud (U.S.) and Microsoft Azure Government, enabling cloud-native security and compliance workflows inside government-authorized environments. These integrations allow agencies to manage authorization, continuous monitoring, and risk controls directly within hyperscaler infrastructure – supporting the shift toward continuous ATO2 and zero-trust models. In practice, this work has enabled federal customers to deploy secure workloads faster while maintaining strict compliance requirements, a growing priority as U.S. government IT moves decisively toward hybrid and cloud architectures.

Beyond hyperscaler alignment, TLS has remained deeply embedded in federal modernization initiatives, supporting defense, civilian, and intelligence agencies as they adapt to evolving cyber threats and regulatory expectations. This combination of long-standing institutional trust and forward-looking software investment defines Telos today – a company reshaped in recent years to translate decades of government expertise into cloud-first, compliance-driven cybersecurity platforms.

—

1 – Telos ID is Telos’s identity verification and enrollment business, focused on large-scale, government-sponsored identity programs.

2 – Continuous Authorization to Operate (continuous ATO or cATO) refers to a modern federal cybersecurity approach in which systems are approved based on ongoing, automated monitoring of security controls rather than infrequent, manual reauthorization cycles. Instead of treating compliance as a one-time event, cATO enables agencies to continuously assess risk, validate controls, and maintain operational approval as systems evolve – supporting faster cloud deployment while preserving security and regulatory integrity.

—

1

Mandate To Secure

Telos operates at the intersection of federal cybersecurity, compliance automation, and identity operations, with a business model built around long-duration government programs rather than transactional enterprise sales. In practical terms, TLS makes money by embedding itself deep within U.S. government workflows where security, accreditation, and trust are mandatory – and where switching costs are high once a provider is established.

The company’s revenue is concentrated in Security Solutions, which now accounts for the vast majority of total revenue, following the deliberate wind-down of lower-growth Secure Networks activities. Within Security Solutions, Telos runs two distinct but complementary engines.

The first is Telos ID, which has emerged as the company’s primary growth engine. This business focuses on operating large-scale federal identity programs, where Telos is responsible for identity proofing, enrollment, and ongoing program execution rather than selling software licenses or discrete services. Flagship initiatives such as TSA PreCheck place Telos directly inside the daily operating flow of government identity systems, with revenue generated as participation and renewals occur over time.

Today, Telos runs these programs across a nationwide footprint of 504 enrollment locations spanning 41 states and Puerto Rico, giving it both physical scale and operational depth. Because TLS functions as the program operator rather than a transactional vendor, growth is largely driven by program adoption, utilization, and longevity, not by chasing new customers. Once established, these programs tend to be multi-year, operationally embedded, and difficult to replace – creating durable revenue streams anchored in federal mandates rather than discretionary IT spend.

The second engine is Xacta, Telos’s cybersecurity and compliance platform. Xacta automates governance, risk, and compliance workflows for organizations operating under strict regulatory regimes, including continuous authorization and zero-trust-aligned environments. Rather than selling generic security tooling, Telos positions Xacta as infrastructure software that translates federal policy and accreditation requirements into operational systems. This creates a SaaS-like revenue profile, with recurring licenses, renewals, and deep integration into customer processes.

Together, Telos ID and Xacta underpin a recurring-revenue model built on two pillars – long-duration federal programs on the identity side, and deeply embedded software subscriptions on the compliance side.

In October 2025, Telos extended this platform with Xacta.ai, embedding AI-driven analysis and automation directly into compliance workflows. Early adoption – including a first enterprise-wide deployment by a U.S. federal agency – suggests Xacta.ai is less about experimental AI and more about productivity gains for overburdened security teams. Over time, this strengthens TLS’s ability to expand wallet share within its installed base, shifting more of the mix toward higher-margin software.

Strategically, Telos aligns its offerings with government-authorized cloud environments, including AWS GovCloud and Microsoft Azure Government, ensuring agencies can modernize infrastructure without breaking compliance. The company also participates in major IDIQ3 contract vehicles, such as the Missile Defense Agency’s SHIELD program, which expand its addressable opportunity set across homeland security, defense, and missile defense modernization – even though revenue remains task-order driven.

From a market perspective, TLS plays inside a large and growing federal cybersecurity and identity ecosystem. U.S. government cybersecurity and identity spending runs into the tens of billions of dollars annually, supported by persistent digitization, zero-trust mandates, and secure identity requirements across critical infrastructure. Telos’s current share of that market is modest, but its embedded program exposure, growing software layer, and institutional trust give it room to expand share organically over time.

Recent U.S. policy under the Trump administration further reinforces these dynamics. Emphasis on national security, domestic infrastructure, and federal IT modernization – alongside restored R&D expensing and other pro-investment measures – indirectly supports companies like Telos that combine U.S.-based operations with mission-critical government programs. Taken together, Telos’s business is not about chasing broad enterprise adoption. It is about owning narrow, high-stakes lanes in federal security and identity, then compounding growth through scale, automation, and software depth once trust is established.

—

3 – IDIQ contract vehicles are U.S. government procurement frameworks that pre-approve vendors for multi-year programs, allowing agencies to issue task orders over time; revenue is earned only when specific task orders are awarded, not from the contract’s headline ceiling.

—

1

Clearing The Beat

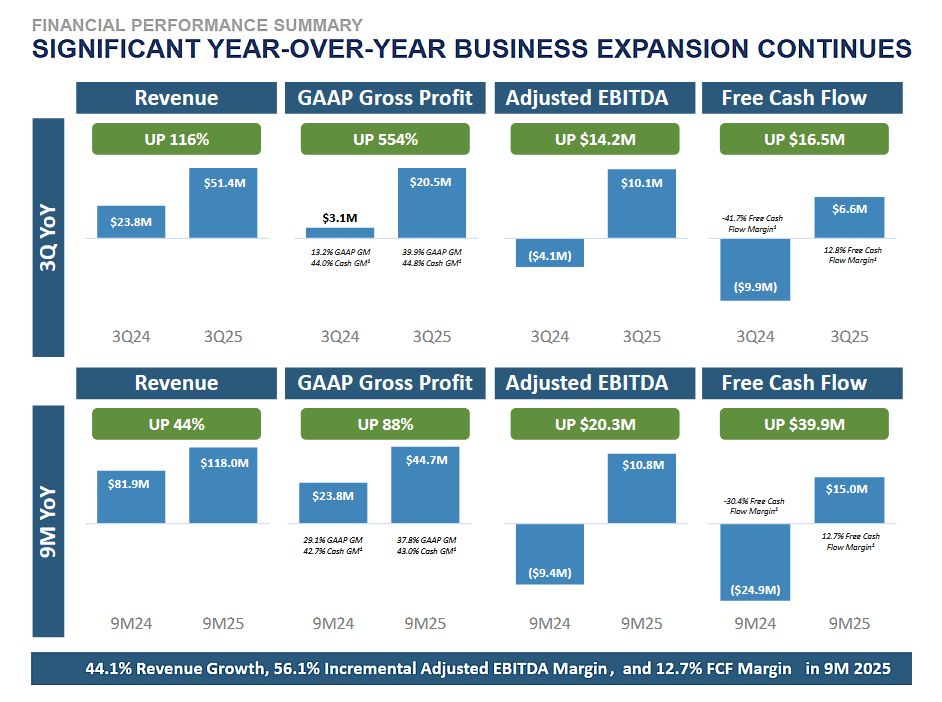

Telos’s financial profile has shifted materially over the past year, moving from uneven execution to a clearer pattern of acceleration and operating leverage. That inflection became especially visible in Q3 2025, a quarter that marked another step-change rather than a one-off spike.

Revenue reached $51.4 million, up 116% year-over-year and well above both company guidance and analyst expectations. It was the company’s eighth consecutive quarter of revenue outperformance, extending a streak built on steady program expansion rather than cyclical demand. Growth was driven overwhelmingly by Security Solutions, particularly Telos ID, while Secure Networks continued its expected decline. The mix shift matters: the company is increasingly growing where margins and recurrence are structurally better.

Profitability improved even faster than revenue. Adjusted EBITDA came in at $10.1 million, nearly double the high end of management’s prior outlook and translating into a 19.6% margin – the strongest since 2018. This was the company’s 14th straight adjusted EPS beat, underscoring a consistent trend of conservative guidance followed by operational overdelivery. Gross margin held up well despite scale, with GAAP gross margin at 39.9% and cash gross margin4 at 44.8%, reflecting both mix improvement and better cost absorption.

Cash flow followed earnings higher. Telos generated $9.1 million in operating cash flow and $6.6 million in free cash flow during the quarter, a notable shift for a company that has historically reinvested heavily ahead of growth. The balance sheet remains clean: Telos ended Q3 with roughly $59 million in cash, minimal debt, and ample liquidity to fund operations and ongoing software development without financial strain.

Telos reached non-GAAP profitability in Q3 2025, driven by scale in Security Solutions and improving operating leverage. GAAP profitability has not yet been achieved, largely due to mix-driven margin variability and ongoing investment, but GAAP losses have narrowed materially. Management has avoided committing to a specific GAAP breakeven quarter, though current trends suggest profitability is a question of timing rather than viability.

Guidance reflects that confidence. For Q4 2025, Telos expects revenue of $44-46.3 million, implying 67-76% year-over-year growth, with cash gross margins moderating modestly to the 40-41% range due to normal mix shifts. Full-year revenue guidance of $162-164 million implies roughly 50% year-over-year growth, slightly ahead of Street expectations.

Taken together, Telos’s financials now tell a more coherent story: accelerating top-line growth, expanding margins, improving cash generation, and a low-leverage balance sheet. GAAP profitability is still a milestone ahead, but the combination of recurring revenue, scale effects, and disciplined execution suggests the foundation is being laid for a more durable earnings profile as growth continues.

—

4 – Cash gross margin is a non-GAAP measure that excludes non-cash costs such as stock-based compensation from cost of revenue, providing a clearer view of Telos’s underlying unit economics and operating scalability.

—

Source: Telos Corporation Q3 2025 Earnings Presentation

1

Delivering Authority

Telos fits within a focused group of U.S.-listed companies that generate durable revenue by embedding technology inside long-duration government programs rather than chasing broad commercial adoption. Its most relevant public peers include OneSpan, a small-cap identity and security software provider navigating a similar transition toward recurring, compliance-driven revenue; Parsons, a growth-oriented federal technology contractor expanding its cyber and digital footprint across defense and intelligence missions; and CACI International, a scaled provider of mission-critical cyber and software solutions for U.S. government agencies. Together, these companies form the most appropriate benchmark set for evaluating TLS’s valuation and stock performance, reflecting shared exposure to federal customers, high switching costs, and business models where trust, authorization, and execution drive long-term compounding.

Through the first half of the year, Telos underperformed larger federal peers as markets favored certainty over upside. Investors gravitated toward scaled contractors like CACI, which offer long-duration, fully funded programs and high earnings visibility during periods of budget and election-related noise. TLS, by contrast, was still viewed as a prove-it story, carrying a heavier execution discount despite improving fundamentals. That dynamic shifted sharply in August. As evidence mounted that Telos’s growth and margin expansion were structural rather than episodic, the stock repriced quickly. The move was not tied to a single catalyst, but to collapsing risk premiums as investors began to recognize the durability of Telos’s program-driven, recurring revenue model. As a result, TLS has outperformed its peer group year to date, rising more than 50%. Despite Telos’s strong rally this year, the Street’s average price target continues to imply nearly 70% upside from current levels.

Even after its sharp re-rating, Telos’s valuation still reflects a company in mid-transition rather than one that has fully arrived. On headline multiples, TLS screens expensive on near-term earnings, a function of its recently emerged non-GAAP profitability and still-modest earnings base. That said, the picture looks more balanced when viewed through a growth-adjusted lens. On forward revenue metrics, Telos trades broadly in line with peers such as CACI and Parsons, and at a premium to OneSpan that reflects faster expected growth and a more programmatically embedded revenue mix. Its forward PEG of about 1.9x – based on conservative consensus growth assumptions – sits roughly in line with CACI and below Parsons, suggesting the market is acknowledging the earnings inflection without fully pricing in longer-term operating leverage. In short, TLS is no longer a deep value reset, but it also does not appear to be stretched relative to peers given its growth trajectory.

Although Telos Corporation approved a $50 million share repurchase program back in May 2022 – which continues to be active with no expiration date – it made limited use of the authorization until recently. Moving away from its cash-preservation mode of 2023-2024, the company is now beginning to deploy its liquidity strength and nearly debt-free balance sheet to return capital to shareholders. In Q3 2025 alone, Telos deployed approximately $3.6 million to buybacks, bringing the total value of shares repurchased over three quarters of 2025 to $7.6 million, equivalent to nearly 3% of the outstanding share count.

With the earnings inflection now visible, federal programs scaling, and capital returns resuming, Telos is transitioning from a re-rating story into an execution story. From here, further upside depends less on sentiment shifts and more on the company’s ability to compound margins and generate cash flow as its programmatic and software engines continue to mature.

1

To Sum It All Up

Telos is a growth story shaped by mandate, scale, and execution rather than hype-driven adoption. What began as a niche government contractor is evolving into a platform company embedded inside the operating fabric of federal security and identity systems. Its growth is structural, anchored in long-duration programs, recurring workflows, and compliance requirements that do not reset with economic cycles. As identity operations scale and compliance automation shifts toward continuous authorization, Telos sits in a position few competitors can replicate – trusted, embedded, and difficult to displace. Recent execution confirms the transition is real, with software depth increasing alongside operational leverage. Yet the market still treats Telos as a transitional story rather than a compounding one. With expanding program scope, deeper software penetration, and rising institutional confidence, Telos is entering its next phase – one defined by durability, not experimentation.

1

1

Smart Growth Portfolio

|

1

1

Disclaimer

The information contained in this article represents the views and opinions of the writer only, and not the views or opinions of TipRanks or its affiliates and should be considered for informational purposes only. TipRanks makes no warranties about the completeness, accuracy, or reliability of such information. Nothing in this article should be taken as a recommendation or solicitation to purchase or sell securities. Nothing in the article constitutes legal, professional, investment and/or financial advice and/or takes into account the specific needs and/or requirements of an individual, nor does any information in the article constitute a comprehensive or complete statement of the matters or subject discussed therein. TipRanks and its affiliates disclaim all liability or responsibility with respect to the content of the article, and any action taken upon the information in the article is at your own and sole risk. The link to this article does not constitute an endorsement or recommendation by TipRanks or its affiliates. Past performance is not indicative of future results, prices, or performance.