TipRanks Smart Growth Portfolio #5: Hardwired Advantage

1

Dear Investors,

Welcome to the 5th edition of the Smart Growth Portfolio and Newsletter.

1

1

Portfolio News and Updates

❖ monday.com (MNDY) announced the appointment of Casey George as Chief Revenue Officer. With nearly 30 years of experience in scaling tech companies, George will lead the company’s growth in the enterprise market, focusing on expanding its global reach and enhancing its go-to-market strategy. The company plans to increase its workforce by 30% in 2025, emphasizing sales team expansion to drive further growth.

❖ Clear Secure (YOU) continued to expand locations outside airports to enroll and renew consumers in the Trusted Traveler program by opening a new location at the Salesforce Transit Center in downtown San Francisco. This marks Clear’s first non-airport location in the area for TSA PreCheck enrollment and renewal services, complementing its 58 airport-based enrollment and renewal locations across the U.S.

1

This Week’s Top Growth Pick: Celestica (CLS)

Celestica Inc. is a global design, manufacturing, and supply chain solutions provider serving advanced technology markets. The company delivers complex hardware platforms and integrated systems for sectors such as aerospace, cloud infrastructure, industrial automation, and healthcare. With capabilities spanning engineering, assembly, and lifecycle management, Celestica helps customers accelerate innovation, reduce time to market, and scale efficiently. Its strategic shift toward high-value segments has expanded margins and deepened exposure to long-cycle growth themes. By combining global manufacturing reach with domain expertise, Celestica plays a critical role in enabling digital transformation across mission-critical industries where precision, reliability, and agility are paramount.

Source: Celestica Inc. Website

1

Rebooted at the Edge

Founded in 1994 as an IBM spinoff, Celestica spent much of its early life as a traditional electronics manufacturing services (EMS) provider, focused on cost-efficient, large-scale production for legacy OEMs. For years, it operated on thin margins in highly commoditized segments, competing primarily on price and volume. But that model began to shift meaningfully in the early 2020s, as Celestica made a deliberate pivot to reposition itself as a high-value, engineering-driven solutions provider.

The inflection point came between 2021 and 2022, when the company began restructuring its portfolio to emphasize complex, higher-margin end markets. It invested heavily in its Advanced Technology Solutions (ATS) segment, targeting aerospace and defense, industrial automation, health tech, and smart energy systems. These sectors require tighter integration, longer product lifecycles, and higher IP content – giving Celestica a strategic edge beyond traditional EMS work.

A key driver of this transformation was the acquisition of PCI Private Limited in 2021, which expanded Celestica’s footprint in Asia and enhanced its design and development capabilities in regulated markets like medical and aerospace. Strategic investments in advanced manufacturing, supply chain orchestration, and digital engineering services further enabled it to move up the value chain. These efforts strengthened Celestica’s position in regulated industries and laid the groundwork for explosive growth in AI-driven networking solutions – a shift that became central to its revenue acceleration.

In parallel, Celestica deepened relationships with hyperscale cloud and datacenter providers through its Connectivity & Cloud Solutions (CCS) segment. It began building next-gen server, storage, and networking platforms at scale, often in direct collaboration with tier-1 customers such as cloud hyperscalers, telecom giants, and top OEMs. These engagements became more design-intensive and stickier, creating longer-term visibility and stronger margins.

Over the past three years, Celestica also ramped up capital allocation into innovation and vertical integration, pushing further into end-to-end services. Today, CLS manages everything from sourcing and production to logistics and aftermarket support – giving it tighter control over costs, quality, and delivery. This full-stack approach has drawn interest from institutional investors focused on nearshoring, supply chain resilience, and industrial reshoring.

By 2024, Celestica was no longer a commoditized EMS player – it had become a strategic manufacturing partner for mission-critical systems in aerospace, cloud infrastructure, and smart industry. This transformation allowed it to win market share, improve earnings quality, and position itself as a growth name riding long-duration technology and infrastructure trends.

Source: Celestica Virtual Investor Meeting, 2024

1

The Backend of Everything

Celestica operates at the intersection of advanced manufacturing, system-level design, and global supply chain integration – building high-complexity, mission-critical hardware platforms for some of the world’s most demanding industries. The company’s operations are anchored in two core segments: Connectivity & Cloud Solutions (CCS), which powers hyperscale datacenters, AI infrastructure, and next-gen networking; and Advanced Technology Solutions (ATS), which serves long-cycle, regulation-heavy markets like aerospace, defense, industrial automation, and health tech.

In CCS, Celestica designs and builds AI-optimized servers, 400G/800G switches, and high-performance storage systems at massive scale. It partners directly with leading cloud providers, networking firms, and telecom OEMs to deliver tailored platforms that meet rising demands for speed, efficiency, and thermal management. This segment has emerged as a key growth engine, benefiting from the AI hardware boom and ongoing cloud expansion.

Meanwhile, ATS provides a stabilizing counterweight, with steady demand from aerospace electronics, medical devices, and smart industrial systems. These customers require not just manufacturing, but regulatory compliance, engineering input, and lifecycle support – areas where Celestica has built credibility for decades. Together, CCS and ATS offer a balanced revenue mix across volatile tech cycles and resilient industrial demand.

Celestica’s value lies in its ability to deliver full-stack solutions – combining product design, engineering, sourcing, assembly, logistics, and aftermarket services under one roof. It thrives in situations where OEMs want to outsource some of the complexities involved but nevertheless retain control over quality, speed, and IP integrity.

Source: Celestica Virtual Investor Meeting, 2024

1

Whether it’s a ruggedized system for a military satellite or a liquid-cooled AI server for a hyperscaler, Celestica delivers full-system integration at scale – with deep domain expertise embedded into every step. Emerging areas like edge computing, digital healthcare, robotics, electrified aviation, and IoT-driven industrial systems are expanding its role as industries digitize from the infrastructure outward.

Celestica’s total addressable market spans across the $600 billion global electronics manufacturing services space. Its core TAM of roughly $150-200 billion – which includes over $50 billion in cloud and AI infrastructure and more than $40 billion in aerospace – grows at 8-10% CAGR, with AI-optimized hardware surging at 15-20%.

Source: Celestica Virtual Investor Meeting, 2024

1

Margin of Execution

Celestica has demonstrated outstanding financial growth over the past three years, with revenue increasing at a CAGR of almost 20% and non-GAAP EPS surging at a CAGR of nearly 54%. Beneath this accelerating growth lies a business model engineered for profitable execution in volatile environments. The company exited 2024 with $423 million in cash, no immediate liquidity constraints, and strong free cash flow generation – $96 million in Q4 alone. Its balance sheet supports ongoing growth without requiring external capital, even as macro and trade headwinds intensify.

Source: Celestica Inc. Investor presentation, January 2025

1

Celestica’s 2024 financial performance was exceptionally strong. Full-year revenue grew 21%, driven by surging demand for AI-optimized infrastructure and next-gen datacenter hardware. Adjusted EPS rose 58%, reflecting both operating leverage and a favorable mix shift toward high-margin programs.

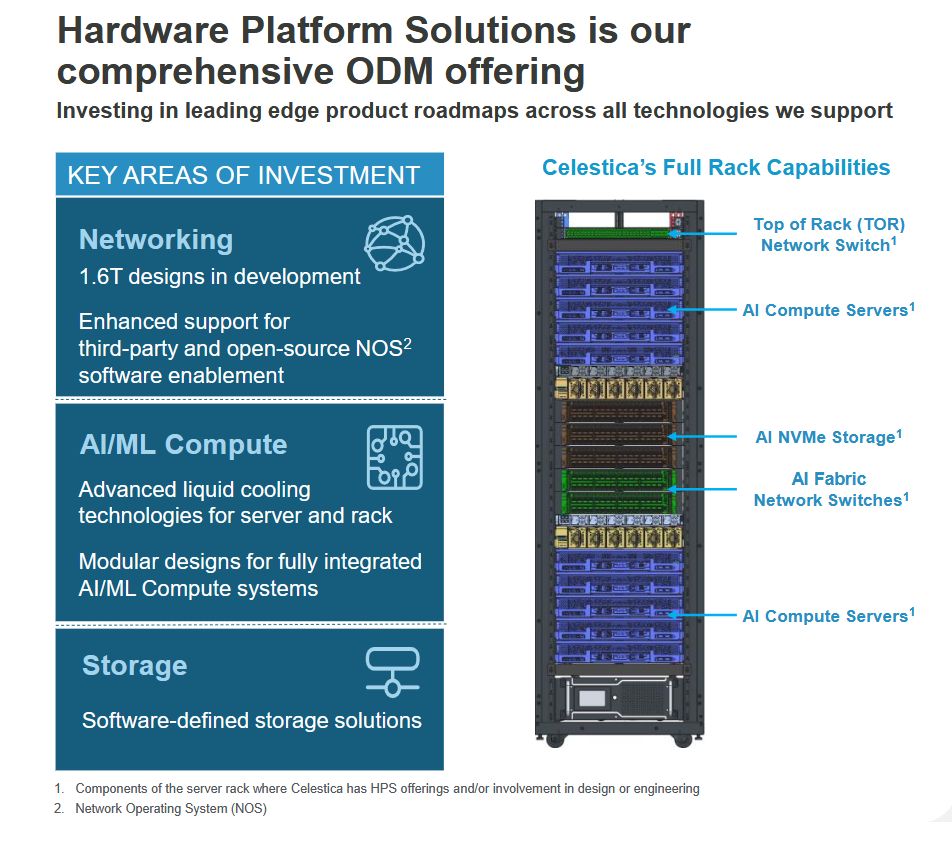

The CCS segment led the charge, growing 30% year over year in Q4 2024 to $1.74 billion. Within CCS, Celestica’s Hardware Platform Solutions (HPS) business – now its primary AI growth vector – jumped 65%, reaching $800 million for the quarter. That growth reflects new wins in ultra-high bandwidth switching, AI servers, and liquid-cooled rack-scale systems for hyperscalers and digital-native clients. Production on these new AI programs ramps in 2026, but revenue visibility is already influencing guidance.

Meanwhile, the ATS segment held steady at $810 million in Q4, with long-cycle demand in aerospace, defense, and medtech offsetting weakness in industrial automation. ATS provides a stable revenue and margin floor, anchoring Celestica as CCS cycles upward with hyperscaler investments.

Celestica expanded its margins across the board, with adjusted operating margin reaching 6.5% – well above the 5% average of its EMS peers. These leadership-tier margins were achieved while transitioning into higher-value segments – AI infrastructure, aerospace, and health tech – without the benefit of software-level profitability. This strength is backed by operating leverage in CCS and a rising return on invested capital, which hit 29.1% in 2024, a multi-year high. Celestica continues to emphasize capital-efficient execution, integrating design, sourcing, assembly, and logistics to compress cost and lead time across its portfolio.

Source: Celestica Inc. Investor presentation, January 2025

1

In Q4 alone, Celestica secured three major AI infrastructure programs that reinforced its leadership in 1.6 Terabyte switching and rack-scale systems. It won a second 1.6T Ethernet switching contract with a top-tier hyperscaler, a third switching program with another cloud giant, and a full AI-optimized rack system deal with a large digital-native customer. These wins, though not yet in production, signal growing customer reliance on Celestica’s design-led manufacturing and advanced cooling capabilities. They also lock in multi-year visibility and reinforce the company’s shift from commoditized assembly to high-value system co-development. CLS’s role in the AI datacenter buildout isn’t just assembly – it is co-designing the hardware that powers it.

This strategic role shift and the strength of its AI program pipeline, along with a healthy backlog, fueled CCS’s growth and underpinned the company’s raised 2025 outlook. Management now guides for $10.7 billion in 2025 revenue and adjusted EPS of $4.75, reflecting YoY growth of 11% and 22%, respectively. Additionally, it pencils in a 6.9% adjusted operating margin and free cash flow of $350 million.

1

Tariffs Meet Tolerance

That financial strength will be tested in 2025, as Celestica faces a new round of U.S. tariffs that could pressure costs and expose vulnerabilities in its global footprint. Although CLS is based in Canada, U.S. clients represent over half of its revenues. Despite its Canadian headquarters and approximately 70% of manufacturing capacity based in Asia, Celestica is less exposed to the sweeping tariffs announced on April 2 than it may appear at first glance. Its flexible footprint and history of navigating regulatory crosscurrents give it an agility that many peers lack.

In recent years, Celestica has actively worked to reduce tariff and trade-dispute risks by expanding operations in Mexico and North America to leverage USMCA trade advantages. It has also increased sourcing flexibility and shifted portions of production and final assembly to preserve compliance and minimize exposure. This geographic adaptability is key to shielding core U.S. contracts from disruption.

Still, CLS is exposed to short-term shocks – particularly related to increased costs for components produced in Asia, which fall outside USMCA protections. However, its vertically integrated model gives it greater leverage over suppliers, which it could use to negotiate price concessions that help offset tariff impacts.

Moreover, the company’s full-stack proposition raises switching costs for clients – increasing the likelihood that they will share in the burden. Its sticky tier-1 customer base – including hyperscalers – may be more inclined to prioritize engineering expertise and delivery assurance over short-term cost volatility, especially given the strategic importance of AI infrastructure in the CCS segment.

In parallel, Celestica’s ATS segment – accounting for over a third of annual revenue – is inherently more insulated from tariff shocks. Long-cycle contracts across aerospace, defense, and health tech, along with rising U.S. domestic demand, provide stability that can help offset volatility in CCS.

In short, while the newly announced tariffs will likely cause some near-term pressure – particularly within CCS – Celestica’s diversified end markets, strong customer entrenchment, and operational momentum offer a meaningful cushion. Its track record of exceeding expectations across nine consecutive quarters suggests it will adapt, even if the adjustment comes with some pain.

1

Deep Value, High Voltage

The expected short-term impact of President Trump’s tariff announcement was immediately reflected in Celestica’s stock. While most of the technology and industrial growth universe opened sharply lower on April 3, CLS was hit harder – deepening a correction that has already shaved off nearly 40% from its February all-time high.

This tariff-induced slide creates a rare setup: a deep-value multiple on a high-growth tech infrastructure player. Analysts are in strong consensus on Celestica’s fundamentals and growth trajectory, making the long-term investment case even more compelling at these levels.

Despite significantly outpacing both the broad Technology sector and EMS peers on revenue, EBITDA, and EPS growth, CLS currently trades at a notable discount to the broader tech index. Relative to its closest comps, Celestica sits in the mid-range on valuation, despite leaving them far behind on revenue acceleration, margin expansion, and multi-year visibility. Its operational momentum and AI-driven growth outlook are in a different league, yet the market hasn’t caught up.

Celestica’s non-GAAP TTM and forward P/E multiples of 18 and 14, respectively, may moderately compress further as markets digest the tariff effects, but they already represent a compelling entry point for long-term investors. Moreover, discounted cash flow models suggest the stock is undervalued by roughly 70%.

Top Wall Street analysts are extremely bullish, rating CLS a “Strong Buy” with a 12-month average price target implying over 110% upside from current levels. Near-term turbulence is likely, but CLS is positioned to outperform over the long haul – driven by strong growth, expanding margins, high-return capital allocation, and a growing role in powering the AI and cloud infrastructure economy.

1

To Sum It All Up

Celestica is a high-growth, high-execution manufacturing and design partner powering the next wave of AI infrastructure, aerospace systems, and industrial digitization. With deep expertise in system-level hardware, thermal engineering, and complex supply chain integration, it delivers mission-critical platforms for hyperscalers and regulated industries alike. The company has shifted decisively from low-margin assembly to full-stack co-development, unlocking margin expansion, multi-year visibility, and market share gains. Its diversified exposure, operational leverage, and capital discipline support strong free cash flow and rising returns. Despite top-tier growth metrics, CLS trades at a steep discount – making it a rare value in deep tech.

1

1

Smart Growth Portfolio

|

1

1

Click here for more stock analysis from TipRanks Macro & Markets research analyst Yulia Vaiman

1

Disclaimer

The information contained in this article represents the views and opinions of the writer only, and not the views or opinions of TipRanks or its affiliates and should be considered for informational purposes only. TipRanks makes no warranties about the completeness, accuracy, or reliability of such information. Nothing in this article should be taken as a recommendation or solicitation to purchase or sell securities. Nothing in the article constitutes legal, professional, investment and/or financial advice and/or takes into account the specific needs and/or requirements of an individual, nor does any information in the article constitute a comprehensive or complete statement of the matters or subject discussed therein. TipRanks and its affiliates disclaim all liability or responsibility with respect to the content of the article, and any action taken upon the information in the article is at your own and sole risk. The link to this article does not constitute an endorsement or recommendation by TipRanks or its affiliates. Past performance is not indicative of future results, prices, or performance.